Cambodia’s small business credit balance touches $36B

Cambodia’s small business credit balance touches $36B

The CBC’s Quarterly Credit Report shows that small business credit performance recorded mixed results, with the number of loan accounts declining marginally, while the total outstanding loan balance continued to grow.

Cambodia’s small business credit balance reached a total of $36.18 billion by the end of the third quarter of 2025, reflecting the total amount of loans that remain outstanding in the Kingdom’s credit market, according to Credit Bureau Cambodia’s (CBC) report released yesterday.

The CBC’s Quarterly Credit Report shows that small business credit performance recorded mixed results, with the number of loan accounts declining slightly while the total outstanding loan balance continued to grow. Loan quality remained stable, and credit demand rose during the period.

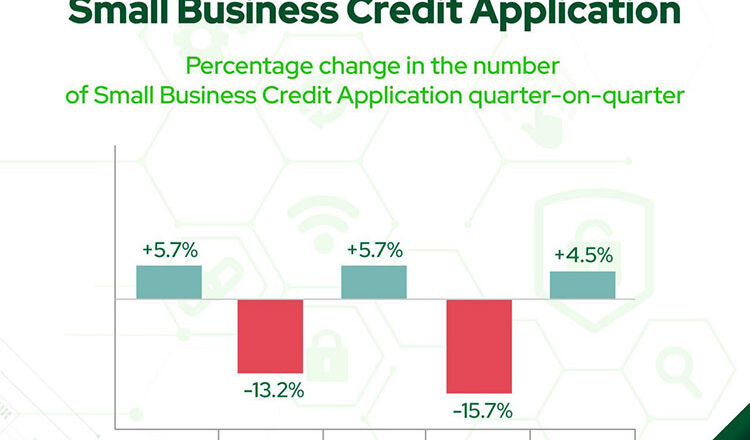

According to the report, small business credit applications increased by 4.5 percent compared to the previous quarter, largely driven by the rise in asset finance and working capital loan applications. Asset finance applications increased by 26.4 percent, and working capital applications rose by 12.2 percent, while “other” loan types declined by 4.8 percent. Construction applications decreased by 7.2 percent, and agriculture applications dropped by 23.1 percent.

The report highlighted that the Plateau region recorded the highest growth, with asset finance applications up by 38.7 percent and working capital applications rising by 18.5 percent. In contrast, the largest declines were seen in Tonle Sap, where “other” applications dropped by 19.7 percent and construction applications fell by 37.9 percent. Agriculture applications saw the biggest fall in the Plateau region, down by 42.6 percent.

In terms of loan amounts, credit applications across all categories increased by 11.8 percent. The rise was mainly supported by asset finance applications, which increased by 32.3 percent, followed by agriculture at 16.5 percent and working capital at 18.8 percent. Meanwhile, construction and “other” applications dropped by 39.6 percent and 3.9 percent, respectively.

The CBC report noted that as of September 2025, the total number of small business loan accounts stood at 1.78 million, a marginal decline of 0.6 percent compared to the previous quarter.

Despite this, the overall outstanding loan balance grew by 1.8 percent, reaching $36.18 billion.

Working capital loans accounted for 52.3 percent of total loan accounts and represented 66.1 percent of the total outstanding loan balance. Agriculture loans made up 29.1 percent of accounts but only 10.4 percent of the outstanding amount. Asset finance loans accounted for 7.5 percent, while construction loans remained minimal at 1.4 percent.

Regional data indicated that the Coastal and Plain regions saw growth in loan balances of 1.4 percent and 2.7 percent, respectively. In contrast, marginal decreases were recorded in the Tonle Sap and Plateau regions at 0.3 percent and 1.0 percent.

In terms of credit quality, the report stated that the 90 days past due (90+ DPD) ratio remained stable at 7.4 percent, the same as the previous quarter. Construction loans recorded the highest delinquency ratio at 11.2 percent, while by region, the highest levels were observed in Tonle Sap at 9.5 percent, Plateau at 9.4 percent, Coastal at 8.6 percent, and Plain at 6.6 percent.

The CBC also reported that 69.8 percent of customers maintained credit relationships with a single financial institution, and 55.5 percent held only one active loan account. Around 30.5 percent of borrowers had two accounts, 10.4 percent had three, and just 3.5 percent held more than three accounts.

“The demand for small business credit increased in this quarter in terms of the number of applications, and we saw the amount of applications increase compared to the second quarter of 2025,” said Oeur Sothearoath, CEO of CBC. “Small business credit performance dropped by 0.6 percent in the number of loan accounts, while the loan balance grew by 1.8 percent. Loan quality remained stable at 7.4 percent for the 90+ DPD ratio.”

The CBC added that while some sectors, such as agriculture and construction, continue to experience slower recovery, overall loan performance remains solid, reflecting Cambodia’s continued economic resilience and financial institutions’ sustained support for small business growth.

- 05:39 14/11/2025