SBV pushes Basel III adoption with new liquidity measure

SBV pushes Basel III adoption with new liquidity measure

The State Bank of Vietnam is accelerating the adoption of international Basel III banking standards by transitioning from the traditional loan-to-deposit ratio to a more stringent credit-to-deposit ratio.

According to a report from ACB Securities (ACBS) on May 8, the proposed transition under draft amendments to Circular No.22/2019/TT-NHNN represents a shift towards a more substance-based assessment of bank liquidity, while offering incentives for lenders that move quickly towards global risk management frameworks.

|

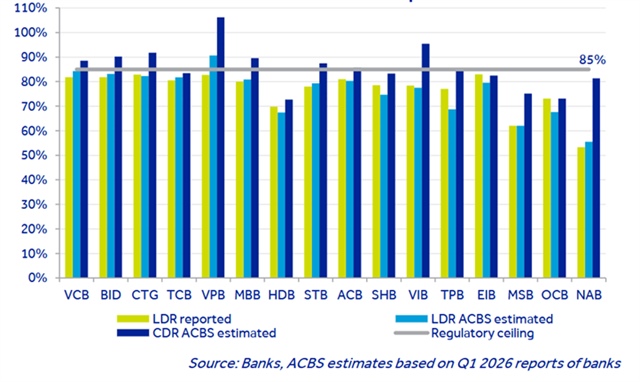

In the new credit-to-deposit (CDR) calculation, corporate bond balances will be added to total credit, while equity is deducted.

On the liability side, interbank deposits, a volatile source of capital, will be excluded. Additionally, only 20 per cent of term deposits from the State Treasury will be counted towards the funding base.

The revised methodology is expected to push the CDR of several major lenders above the regulatory ceiling of 85 per cent. ACBS analysts suggest that VPBank, VIB, MB, VietinBank, BIDV, and Sacombank, could see their ratios exceed the cap if their capital structures remain unchanged.

The State Treasury’s deposits at the banking system totalled $25.07 billion at the end of March. State-owned lenders hold approximately 99.6 per cent of this amount, or $24.97 billion, making them particularly sensitive to the new treatment of treasury funds.

As of March 31, the loan-to-deposit ratios of Vietcombank, VietinBank, and BIDV stood at 84.5 per cent, 83.5 per cent, and 82.9 per cent respectively, nearing the current limit.

Source: ACBS |

To cushion the impact and encourage modernisation, the State Bank of Vietnam (SBV) has introduced an incentive for early adopters of Basel III standards.

Accordingly, banks that demonstrate 100 per cent compliance with the liquidity coverage ratio (LCR) and Net Stable Funding Ratio (NSFR), both under Basel III frameworks, will be exempt from complying with the CDR.

The LCR measures a bank’s ability to meet 30-day net cash outflows with high-quality liquid assets, while the NSFR measures sustainable funding for long-term credit activities. While mandatory compliance is set for the start of 2028, the SBV is allowing banks to register for early application immediately.

ACBS analysts believe the overall impact on system liquidity will be limited as the SBV provides a flexible choice between standard ratios and Basel III-based frameworks. The shift is ultimately designed to harmonise the domestic banking sector with international practices, ensuring long-term stability and resilience against market shocks.

“The new framework also helps reduce reliance on the more ‘mechanical’ prudential rules previously applied, particularly the short-term funding for medium- and long-term lending ratio. As a result, medium and long-term deposit rates, which currently remain elevated at around 8-9 per cent at many banks, could see additional room for moderation in the upcoming period,” ACBS added.

- 12:09 12/05/2026