Banking sector growth to moderate in 2026

Banking sector growth to moderate in 2026

After a year of strong growth in 2025 the banking industry is expected to deliver a “moderately positive” performance this year, with profits projected to increase by 16 per cent, according to a report by S&I Ratings, a provider of credit rating services, market research and corporate analysis in Việt Nam.

A bank branch in HCM City. The banking sector is expected to achieve 16 per cent profit growth in 2026. — VNS Photo |

Last year, despite the net interest margin (NIM) being hit by liquidity pressures, the sector recorded robust profit growth of 18.9 per cent, driven by strong credit expansion and a recovery in non-interest income, it said.

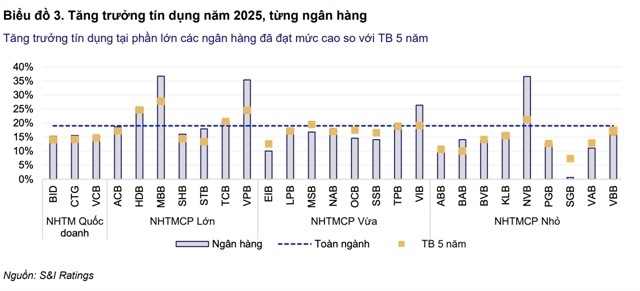

Banks saw improved retail credit growth, primarily driven by a surge in mortgage lending.

But most lenders shifted their focus towards corporate clients, particularly large enterprises and foreign-invested companies, to sustain growth.

Asset quality across the sector also improved significantly, with the non-performing loan ratio declining for three consecutive quarters to end the year at 1.85 per cent.

NIM dropped to 3.1 per cent from 3.4 per cent in the fourth quarter of 2024, the lowest level in several years.

The service fee income rose by 12 per cent in 2025, rebounding after two consecutive years of negative growth.

The main driver of non-interest income came from recoveries of previously written-off bad debts.

Income from other activities, mainly bad debt recoveries, reached over VNĐ58 trillion (US$2.2 billion) to account for 34 per cent of the industry’s total non-interest income.

Real estate credit expected to cool

The banking sector is expected to continue benefiting from the Government’s ambitious economic growth targets in 2026, though admittedly, challenges remain.

The State Bank of Vietnam (SBV) has a credit growth target of 15 per cent, lower than the 19.1 per cent in 2025.

Notably, new regulatory measures include quarterly monitoring of credit growth and a requirement that real estate lending must not grow faster than banks’ overall credit.

“We believe real estate credit growth in 2026 will enter a phase of cooling and more selective expansion rather than maintaining the strong growth seen in 2025,” the report noted.

“But the real estate sector will still remain a significant contributor to loan growth.”

It added that policy moves by the central bank in this area should be closely monitored due to their potential impact on the sector’s growth outlook.

Differences in credit growth quotas between banks are also becoming more pronounced under the SBV’s cautious regulatory approach.

A bank branch in HCM City. The banking sector is expected to achieve 16 per cent profit growth in 2026. — VNS Photo |

Banks involved in restructuring weak financial institutions were granted higher credit growth quotas, while most others were allocated more modest rates of 11–13 per cent at the beginning of the year.

With the economy’s demand for capital remaining high, room for further credit could become a precious resource in 2026, particularly for real estate lending.

Apart from differences in scale, the structure of loan tenors is also creating pressure on funding demand.

In 2025, banks restructured their asset portfolios toward longer-term lending to improve asset yields and support NIM amid margin compression. This increased the ratio of short-term funds used for medium- and long-term lending, thereby raising funding needs.

Liquidity has been strongly supported through the SBV’s open market operations (OMO) and State Treasury deposits, with support through them rising to record levels.

State Treasury deposits at state-owned commercial banks topped VNĐ406 trillion by the end of the last quarter of 2025, while outstanding OMO operations regularly remained above VNĐ200 trillion.

But interbank interest rates have remained significantly higher than OMO rates, indicating a persistence of liquidity pressures.

Taking these factors into account, S&I Ratings forecasts NIM to decline slightly to around 3 per cent in 2026, though performance will vary between banks.

Banks with high current account savings account ratios, lower funding costs and stronger risk management capabilities are expected to stabilise their NIM earlier, thanks to better resilience against interest rate fluctuations.

Banks that rely heavily on higher-cost market funding may continue to face prolonged margin pressure.

“We maintain a moderately positive view on the banking sector for 2026, forecasting industry-wide pre-tax profit growth of around 16 per cent year-on-year,” the report added.

- 08:52 13/03/2026