Loan-to-deposit ratio normalising in 2024, say bankers

Loan-to-deposit ratio normalising in 2024, say bankers

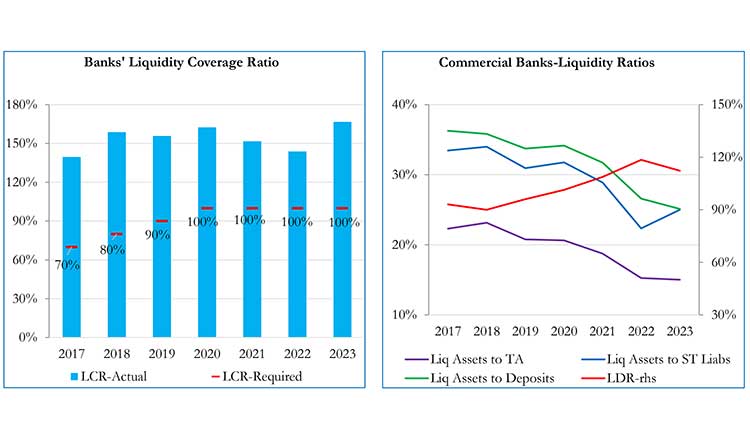

A number that might be of concern in Cambodia’s banking system is its loans versus deposits. For 2023, Cambodia’s banks total loans outstanding was $57.6 billion and total deposits $47.9 billion. Worldwide, the accepted industry norm for safety is to have a loan-to-deposit ratio (LDR) of 80-90 percent. Or at the maximum 100 percent, which would mean for every one dollar the bank is giving out in loans it is having one dollar as a deposit.

But some Cambodian banks on average seem to have a loan-to-deposit ratio of 120 percent; which would mean that for every 100 dollars its having as a deposit, it’s loaning out 120 dollars.

Pointing to an over-leveraged situation as the gap between loan and deposits is nearly at $10 billion ($9.7 billion to be exact).

Credit growth was up only 14 percent against a deposit growth of 21.3 percent in 2023. “As the market matures one cannot expect to see credit growth at 20 percent, which was the norm earlier.

Going forward, one can expect bank loan growth of about 10 percent,” Rath Sophoan, CEO, Maybank and Chairman, Association of Banks in Cambodia (ABC) told Khmer Times.

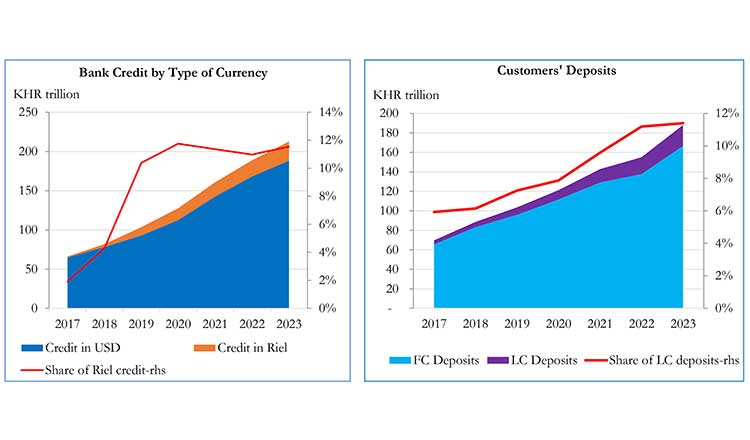

In some part, Cambodia’s dollarised economy is also to blame. Given the US Federal Reserve raised its interest rates 17 times in the last two years. Market participants say the unusually high interest rates (from 6-8 percent for 12-month tenor) being offered last year by banks is a result of this. Banks were more eager to attract deposits last year. But the situation has more or less corrected this year, with many banks lowering their interest rate to between 5.2-5.8 percent.

Industry players say banks have realised an LDR as high as 120 percent is unsustainable in the long run and have reined in their lending. Some banks were forced to use their capital reserves and foreign-owned banks had to borrow from their parent banks’ overseas. NBC in its report said, “Capital adequacy remains healthy, though credit risk has been rising.” In 2024, industry players say that many banks with LDR between 110-120 percent have managed to lower their LDR to safe levels of 100 percent.

For 2023, NBC in a report noted, “NPLs have posted a sharp increase, with specific provision rising in tandem.” NPL rate was as high as 5.4 percent. Market participants say that because borrowers could not repay their loans, there were NPLs. Again for a bank to have interest rates as high as 6-8 percent in 2023 was not sustainable; as doing so would increase the cost of funds; which would in turn impact the lending rate and the banks’ customers.

So with course correction in 2024, there has been more prudent lending by the banks; which would get reflected in 2024 bank performance, said market players. Some felt that currently the country has too many financial institutions – banks and MFIs – making it an over-saturated and competitive market. Market players feel that stronger supervision is required as there is quite a difference in lending practises between the larger banks and the new, loss-making smaller ones.

Market participants say that the larger banks have increased their inter-bank lending activities, which is mopping up their liquidity. It’s smaller banks that continue to face high liquidity, coupled with lower credit growth demand, said industry experts.