Local real estate sector allures foreign investors

Local real estate sector allures foreign investors

Though the foreign direct investment flow into real estate sector accounts for only 5.3 per cent of the total in the first half of the year, experts see the flow is at a more feasible stage.

In the first half of this year, 25 new projects were licensed in Vietnam’s real estate sector with total investment capital up to more than $600 million.

Notable projects include Samsung’s $300 million 21-storey building in Hanoi, a $300 real estate complex project in Hanoi of TNR Holdings and a Russian partner, and Singapore-backed SynGience’s $18 million investment in DepotMetro Tower – Tham Luong.

According to Marc Townsend, managing director of CBRE Vietnam, the FDI flow into real estate has mostly been on the essential demand of accommodation such as housing and apartments, instead of hospitalities, golf courses and retail as previously.

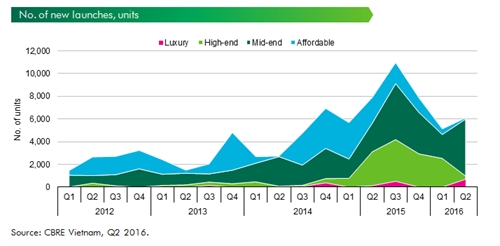

Especially, Vietnam’s real estate sector is attracting interest from Japan and a range of projects are being developed through the co-operation between Vietnamese and Japanese investors in mid-end housing development instead of high-end and luxury segments.

Foreign investment flow has also been seen through a range of merger & acquisition cases. In many cases, the seller of one had become the buyer of another. “This means that the M&A activity was asset transactions for benefit, but not showing the evidence of less attractive real estate to foreign investors,” Marc commented.

CBRE also cited that international developers are becoming much more careful before deciding to pour their investment into Vietnam’s real estate market.

Sigrid Zialcita, executive director of the research division at Cushman & Wakefield in Asia Pacific said that Circular 06/2016/TT-NHNN dated May 27, 2016, which tightens the use of short-term capital sources for medium and long term lending, would bring more foreign investment into this sector.

“With a higher risk weightage attached to real estate loans, one way around it is to raise a company’s equity base. The need for capital injections is an opportunity for foreign investments to gain exposure to Vietnam,” Zialcita said in her recent visit to Vietnam.

“The recent relaxation of the 49 per cent cap in Vietnamese public companies will also be conducive to an increased level of foreign capital into the country. But this means that companies will have to be more transparent as generally, some due diligence would be required,” she cited.

Zialcita took the example of two real estate developers that have so far decided to extend foreign ownership to 60 per cent. One of them, Hoang Quan Consulting, Trading and Real Estate Services, had seen strong interest from investors in Asia, and wanted to become more transparent. Meanwhile Thu Duc Housing Development Corp., will divest from non-core businesses such as cargo handling because the legal foreign ownership limit for these sectors remain around 50 per cent.

According to Zialcita, in order to attract more FDI, Vietnam’s property market needs more transparency, a better legal framework which will result in a more liquid market and thus, more efficient prices which better reflect value. Real estate developments also need to be better aligned to overall economic objectives as well as urban planning guidelines.

In a study carried out by Financial Times data division FDI Intelligence, Vietnam ranks among the top in terms of greenfield FDI into Asia.

Its demographic profile, rapid urbanisation, growing middle class, rising incomes, status as a manufacturing hub, infrastructure developments and stable political climate are attractive fundamentals.

The potential upside, from a higher level of economic integration, is also compelling.