The rise of the landed property sector

The rise of the landed property sector

The landed property sector is outperforming other segments to become Vietnam’s most attractive investment channel.

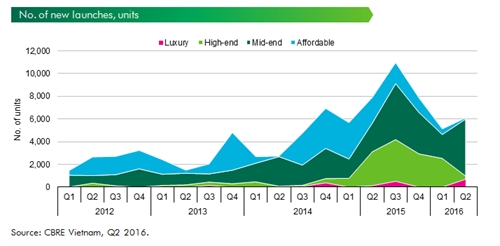

In the latest report by Savills Vietnam, the landed property sector had its best performance ever, with 820 sales in Ho Chi Minh City in the second quarter of 2016, showing growth of 81 per cent quarter-on-quarter (QoQ) and 110 per cent year-on-year (YoY).

Smaller townhouse s have provided affordable housing for a new generation. Townhouses can compete with apartments as they are not that much more expensive yet offer far greater advantages, such as recreational amenities, pools, on site education facilities, convenient shopping, and the security of a gated community.

The Sapphire development, with a range of niche residential to large-scale commercial projects, has recently entered the landed property segment, with 29 riverfront villas at HOLM project.

David Clarkin, joint managing director of Sapphire, told VIR that there had always been a global desire for individuals to own their own piece of land and home, Vietnamwas no different.

The population of Ho Chi Minh City has increased from approximately three million to eight million people over the past 30 years, the opportunity to acquire well located residential land is rapidly diminishing. This makes landed property all the more desirable, according to Clarkin.

The problem for developers lies in the finite availability of land in the most desirable residential areas for villas and townhouses. Indeed, this asset class has come of age and now has critical supply mass. A city such as Ho Chi Minh has an almost infinite ability to construct high-rise apartment buildings adding a large amount of units to the market. However, the opportunity to build villa projects, within the inner suburban neighbourhoods, is rare.

“The limited supply, coupled with greater demand from the increasingly wealthy middle classes will result in above average capital growth in the landed sector, when compared to other segments,” he stated.

With the same view, Matthew Koziora, director of Transactions at VinaCapital, said that townhouses and villas offered local buyers a number of features that condos did not, including greater liquidity. With the forward supply of landed property probably one-twentieth of condos, their ability to re-sell prior to handover surpasses that of condominiums.

He pointed out that the main difficulty for new landed projects was finding good sites with approval in place. Lower forward supply will therefore create a more sustainable market in terms of liquidity and saleability.

Local buyers are becoming increasingly price sensitive, they want value for their money. They are also looking for quality designs and facilities with close proximity to amenities, according to Koziora.

VinaCapital’s recent launches have been quite successful, including its latest project, 9 South Estates in Saigon South, which has recorded robust sales over the past five months due to its impressive list of on-site facilities.

Troy Griffiths, deputy managing director of Savills Vietnam is bullish on the prospect of the landed segment.

“Historically, a townhouse in Ho Chi Minh City was three times as costly as a high-end apartment. However, this has now reduced to 1.7 times in newly developed areas. This is a low step ratio that shows landed property is well within reach for many,” he said.

The local landed property market promotes sustainability because of a healthy purchaser structure. End-users account for the majority of purchasers, with speculators less than 10 per cent. Investors are abundant in the townhouse segment, prompting an expansion of the rental market in the near future. Thus, townhouses have outperformed other residential asset classes in investment returns, thanks to land value appreciation and stable rental returns.

Savills Vietnam forecasts that the landed property demand in 2016 would be YoY 103 per cent higher in Ho Chi Minh City and 88 per cent higher in Hanoi, supported by a growing affluent class. Compared to regional peers with similar population densities, such as Kuala Lumpur, Bangkok and Jakarta, Ho Chi Minh City and Hanoi’s primary supply of landed housing (less than 10 per cent) is relatively small, leaving ample room for future growth.