Vietnam in 2023: Facing a recession or a rebound?

Vietnam in 2023: Facing a recession or a rebound?

Vietnam will once again face an uncertain world economy in 2023: high inflation will hurt the real incomes of consumers and depress retail sales in many countries, rising interest rates will cool down housing markets, and property developers will postpone new housing construction, China’s difficult exit from the pandemic will impair growth in the short term; and geopolitical tensions will induce more volatility in energy, food, and financial markets.

Thankfully, the International Monetary Fund (IMF) and Organisation for Economic Co-operation and Development (OECD) predict that the world economy will avoid a recession in 2023 – but just barely. The OECD projects global GDP growth of 2.2 per cent in 2023, while the IMF projects growth of 2.7 per cent. These average growth rates conceal large differences between groups of countries.

Patrick Lenain - Senior associate Council on Economic Policies

Activity in advanced economies will stagnate, as their central banks fight elevated inflation rates with further tightening of monetary policy.

US inflation has fallen in recent months. With seven interest rate hikes in 2022, the US Federal Reserve has increased its rate to the 4.25-4.5 per cent range, the highest in seven years. More hikes will be necessary to bring inflation under control, thus holding back growth.

Europe has also seen a tightening of monetary policy. Nonetheless, euro area inflation remained relentlessly above 10 per cent in November – also exceeding the official target of 2 per cent by a large margin.

The European Central Bank (ECB) has been cautious with its fight against inflation, and its main refinancing rate reaches only 2.5 per cent, not high enough to push back price pressures. Monetary tightening, high inflation, expensive energy, and ongoing uncertainty will all weigh down on European growth in 2023.

The fog of war in Ukraine clouds Europe’s outlook with recurrent threats of disruptions, dislocating relations with Russia, and potential new refugee crisis. The OECD projects that the euro area will expand by only 0.5 per cent in 2023.

By contrast, emerging Asia will be an engine of global growth in 2023. The countries will remain resistant to global headwinds and will see only a modest and short-lived overshooting of inflation. According to the latest OECD projections, Two-thirds of global economic growth will come from emerging Asia, with particularly strong growth in India (6 per cent), Philippines (5 per cent), Indonesia (4.9 per cent), Malaysia (4.4 per cent), and Thailand (3.7 per cent).

How strongly China will grow is much debated. The IMF and OECD have revised down the country’s growth projection to 4.6 per cent in 2023, well below the rapid pace reached in the past decade, and the World Bank recently cut it down further to 4.3 per cent.

The country is only now reopening from the pandemic at a fast pace. The experience in other countries, in an environment of incomplete vaccination, suggests that infections will rise sharply. This will lead to a voluntary reduction in social interactions until the health situation normalises.

Once herd immunity is reached, fears of infections will wane, and economic activity will resume. The rebound is expected in the second quarter of 2023, but how pandemics evolve over time is particularly difficult to predict.

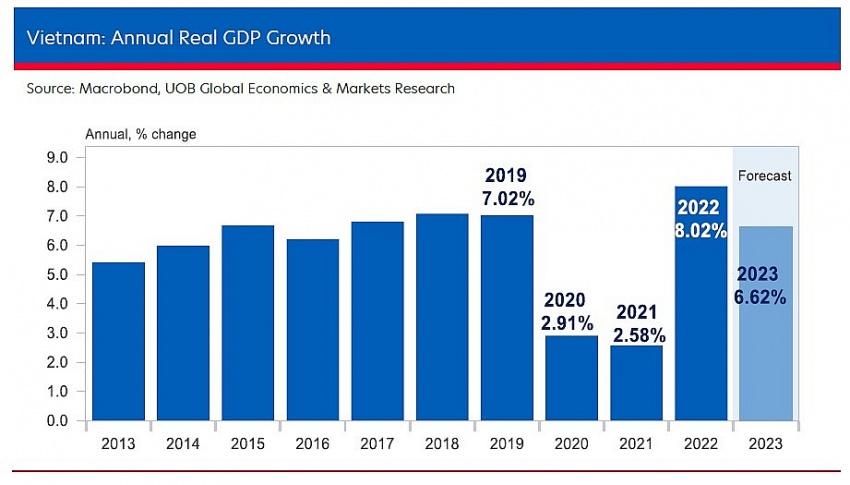

Like elsewhere in emerging Asia, strong growth is projected to continue in Vietnam. The IMF projects activity to expand by 6.1 per cent, the World Bank expects growth of 6.4 per cent, and the Asian Development Bank projects an expansion of 6.7 per cent. This will put Vietnam among the fastest-growing economies in the world. This upbeat growth outlook owes a lot to the well-managed exit from the pandemic, with an early decision to vaccinate the population and lift all restrictions, thus allowing an early return to normal activity.

Vietnam’s inflation has increased, but it exceeded the official target (4 per cent) by only a small margin in November (4.37 per cent). Cautious hikes of interest rates by the central bank are welcome to keep inflation under control and retain confidence, without jeopardising the pace of growth.

The State Bank of Vietnam (SBV) should remain vigilant as inflationary pressures could build up, especially if exchange rate depreciation passes through to import prices and feed upward inflation in coming months. The goal of monetary policy should be to bring back inflation to the official target within a reasonably short time frame.

Keeping a fast growth momentum while the global economy weakens will be challenging. Exports are a traditional driver of Vietnam’s growth, but exporters will face weak demand from customers in North America and Europe.

Foreign direct investment is also a traditional driver of Vietnam’s growth – with many success stories in electronics. New announcements by Samsung, LG, Foxconn, and Lego testify to Vietnam’s ongoing attractiveness. However, multinational enterprises now face pressure to re-shore production, boost job creation in their home countries, make supply chains more resilient, and strengthen national security. This could weaken foreign investment inflows in years to come.

Real estate property investment has also been a key driver of growth in recent years – though with great financial risks. Low-interest rates and easy credit conditions fuelled a property boom, with fast-rising housing prices. Now that the SBV is hiking interest rates and tightening credit to fight inflation, the housing price cycle is coming to an end.

A similar pattern is observed in housing markets around the world: residential property prices in China have been on the decline over the past two years, with some property developers in dire financial distress. US house prices have declined since mid-2022, reflecting the rise in mortgage rates.

Vietnamese homebuyers will be more cautious going forward, and developers will postpone new home construction in a frozen market. This will choke off an important engine of growth. Investment to decarbonise the economy can become a key growth driver in the short and medium term. Vietnam has made the pledge to achieve carbon neutrality in 2050. This does not leave much time to make the large investments required to cut emissions.

Despite more solar panels and wind turbines, coal remains the mainstay of Vietnam’s power sector and is the largest contributor to greenhouse gas emissions. These projections depict an optimistic outlook of strong growth and cooling inflation. But rarely has it been so difficult to make forecasts. Vietnamese companies and consumers should be ready for new shocks, and potentially a new crisis.

Much higher interest rates in high-income countries would entail a return of capital flows to high-yield markets and safe havens, which would put under pressure the currencies of emerging economies such as Vietnam.