Fiscal reforms a must to underpin growth

Fiscal reforms a must to underpin growth

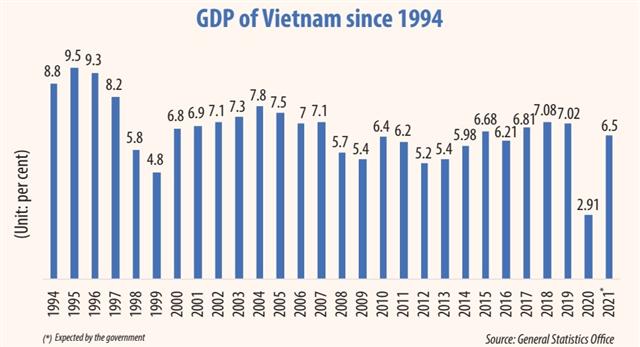

Despite no signs of an end to the pandemic, the government is expecting a growth rate of 6.5 per cent this year. Francois Painchaud, resident representative of the International Monetary Fund in Vietnam, writes about what the country should do to achieve its 2021 target, especially in terms of fiscal and monetary policies.

Francois Painchaud, resident representative of the International Monetary Fund in Vietnam

|

Vietnam took decisive steps to contain the COVID-19 pandemic, which helped limit the health and economic fallout from the health crisis. Swift introduction of containment measures combined with aggressive contact tracing, targeted testing, and isolation of suspected cases helped contain new infections. Fiscal policy also provided support to vulnerable households and businesses.

Measures taken by the State Bank of Vietnam (SBV) lowered the cost of borrowing and facilitated the continued flow of credit. Real GDP growth reached 2.91 per cent in 2020, among the highest in the world. We expect strong recovery in 2021. Growth is projected to strengthen further to 6.5 per cent as normalisation of domestic and foreign economic activity continues. Inflation is expected to remain close to the authorities’ target at 4 per cent.

However, the outlook is subject to substantial uncertainties. Renewed outbreaks, a protracted global recovery, and ongoing trade tensions are amongst the downside risks to the Vietnamese outlook. On the upside, deployment of an effective vaccine or therapy could boost confidence and growth prospects.

Given these uncertainties, the government and the SBV may need to adjust flexibly their policies. Fiscal policy should play a larger role in the policy mix if downside risks materialise, especially given the available fiscal space.

|

Fiscal support should be maintained in 2021, with improving efficiency in execution as priority. Over the medium-term, the emphasis should be on mobilising revenue for financing green and productive infrastructure, strengthening social protection systems, and safeguarding debt sustainability. Monetary policy should remain supportive in the near term. Greater exchange rate flexibility would reduce the need to build forex reserves and facilitate the adjustment to a potentially more challenging external environment. The authorities’ commitment to gradually modernise its policy frameworks is very welcome.

The SBV has struck an appropriate balance between supporting the recovery and banking system resilience. Close monitoring of risks in the banking sector remains crucial. Non-performing loan recognition and loan classification rules should be gradually normalised. Banks’ capital positions need to be further strengthened and capital markets developed to improve financial resilience and promote long-term financing.

Continued structural reforms will be required to support robust and inclusive growth. Priority should be given to reducing the regulatory burden faced by domestic private firms, improving access to land and financial resources, particularly for small- and medium-sized enterprises (SMEs), and reducing corruption. Establishing an expedited SME-specific insolvency regime would help unlock capital and prevent unnecessary liquidations. Reducing labour skill mismatches, increasing human capital, and technology access would also boost labour productivity.