Pandemic enables new leasing trends in Hanoi: Savills

Pandemic enables new leasing trends in Hanoi: Savills

For the first time, landlords in the Old Quarter have to negotiate lease prices with tenants.

The pandemic has reshaped commercial leasing and driven new trends in Hanoi, according to representatives of Savills, one of the world’s leading property agents.

Many shops in the Old Quarter closed due to impact by the pandemic. Photo: Vietnammoi

|

Do Thi Thu Hang, director of Savills Hanoi Advisory Services, attributed the situation to extended uncertainty in the global health crisis and extensive opportunities in e-commerce.

Hang went on to say that uncertainty from Covid-19 has delayed many new project openings while growth in online shopping driven by the rapid change in consumer behaviours requires more innovative customer growth and retention strategies from traditional retailers and landlords.

The market is expanding to the Eastern and Western areas, Hang added.

Meanwhile, Le Tuan Binh, head of Commercial Leasing, Savills Hanoi, said Hanoi retail market vacancy rates in shopping centers and prime locations continue to grow, especially in the Old Quarter where supply has significantly increased.

Binh provided insights into pricing levels and operating capacity by noting that landlords in the Old Quarter for the first time have to negotiate lease prices with tenants.

Le Tuan Binh, Head of Commercial Leasing, Savills Hanoi. Photo: Savills

|

“Landlords need to acknowledge two points to align with current demand. The first is the rental price. As most landlords in the Old Quarter never have had to negotiate prices with tenants, they tended to select whoever bid the highest. However, now we’re seeing proposed pricing that aligns with market reality,” he commented.

The second point is the need for more flexible leasing. Previously, landlords tended to offer more limited rental options, but have since become far more flexible, sub-dividing premises to provide more smaller-sized options. Lease term conditions and rental price adjustments have become more fluid. Although revenues have declined, they will soon recover post-pandemic, Binh said.

Reality in Hanoi

According to the General Statistics Office (GSO), retail sales of goods in Hanoi increased 9.9% on-year in the first half this year thanks to increasing demand for essentials and rapidly developing e-commerce.

However, limited imports and pandemic-caused impacts on income and purchasing power have resulted in low sales.

A recent Savills research found approximately half of retail business revenues have fallen by up to 50% during the extended Covid-19 episode. With demand so heavily affected, it has become impossible for companies and retailers to realise existing planning goals.

Hanoi office market in the first quarter 2020. Source: Savills

|

Changes

The situation prompts changes and landlords need to make adjustments to support businesses and retailers. As a result, leasing price pressure ease has been recorded in recent months.

Compared with pre-pandemic levels, the cost of CBD retail space has fallen significantly; some prime locations have reduced rents by up to 40% to retain tenants.

Despite lease support by owners, shopping center vacancies are still rising. The first aspect is rental strategy. Retailer business strategies are evolving as many recognize the potential e-commerce has to their business. Physical business premises are no longer the number one priority, so shopping centers need to adjust tenant targets, leasing requirements and areas, to attract the most suitable tenants,Binh explained.

Although most retailers have been affected by the pandemic, the Savills research found sales have increased by over 20% in supermarkets. These retailers receive preferential rents compared to others.

Needing larger areas, they also drive footfall and by doing that, attract other retailers; supermarket has become a ‘must-have’ anchor-tenant in any shopping complex.

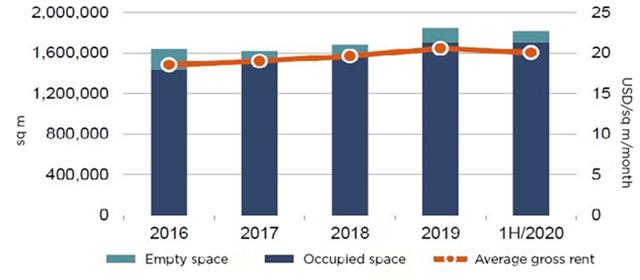

While retail remains deeply affected, the office market remains stable with 95% whole market occupancy and rental prices mildly fluctuating 1-2% on-quarter and on-year.

With leadership businesses tending to have longer-term strategies, Grade A office pricing in the CBD at over US$30 square meter per month has remained high. Furthermore, with grade A tenants mostly being global companies with risk funds, any rental assistance requests tend to be limited to the short-term, Binh said.