Eximbank assigned 'B+/B' and 'axBB/axB' ratings; outlook stable

Eximbank assigned 'B+/B' and 'axBB/axB' ratings; outlook stable

Overview

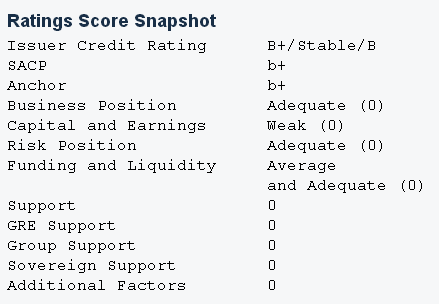

Eximbank has an "adequate" business position, "weak" capital and earnings, "adequate" risk position, "average" funding, and "adequate" liquidity.

We assess the Vietnam-based bank's stand-alone credit profile to be 'b+'. We are assigning our 'B+/B' issuer credit rating to Eximbank. We are also assigning our 'axBB/axB' ASEAN regional scale rating to the bank.

The stable outlook reflects our expectation that Eximbank will maintain its financial profile and temper growth amid difficult operating conditions in Vietnam.

Rating Action

On Nov. 16, 2012, Standard & Poor's Ratings Services assigned its 'B+' long-term and 'B' short-term issuer credit ratings to Vietnam Export Import Commercial Joint Stock Bank (Eximbank). The outlook on the long-term rating is stable. We also assigned our 'axBB' long-term and 'axB' short-term ASEAN regional scale ratings to the bank.

Rationale

Standard & Poor's bases its ratings on Eximbank on the bank's "adequate" business position, "weak" capital and earnings, "adequate" risk position, "average" funding, and "adequate" liquidity, as our criteria define those terms. We assess the bank's stand-alone credit profile to be 'b+'.

Our bank criteria use our banking industry country risk assessment (BICRA) economic risk and industry risk scores to determine a bank's anchor, the starting point in assigning an issuer credit rating. The anchor for a commercial bank operating only in Vietnam is 'b+'. The BICRA score is based on our evaluation of economic risk, given Vietnam's low-income economy, developing financial system, and evolving policy framework. The risk of economic imbalances is high and the credit risk is extremely high, in our opinion, reflecting rapid credit growth--although moderating--together with low income levels, high private sector credit, and rudimentary underwriting standards. Regarding our industry risk assessment, Vietnam's regulatory standards lag international norms and the central bank is prone to regulatory forbearance. The banking system has a moderate risk appetite, overcapacity, and market distortion. An adequate share of core customer deposits and a low reliance on external funding partially mitigate these weaknesses.

Eximbank's position as one of the largest privately owned banks, with a deposit market share of about 2%, supports its business position. The bank has an established franchise in the small and midsize enterprise segment and has increased its presence in the consumer segment, particularly in Ho Chi Minh.

The bank benefits from the strategic alliance and cooperation with its 15%

foreign strategic stakeholder, Sumitomo Mitsui Banking Corp. (A+/Negative/A-1), through the transfer of best practices in the areas of risk management, banking operations, and human resource management. We assess Eximbank's business diversity to be adequate, although the bank has a domestic focus. Interest income contributes most of the bank's earnings. We view the Eximbank management's growth strategy to be aggressive. We expect the government's efforts to stabilize the banking system to result in a more balanced growth strategy for the bank.

We view Eximbank's capital and earnings as a neutral rating factor. We expect the bank's risk-adjusted capital ratio before diversification adjustments to remain about 3.5%-4% in the next 12-18 months. Our view is based on our expectation that Eximbank will moderate its risk asset growth in line with government policy.

Eximbank's relatively straightforward business model supports our view that the bank's risk position is "adequate." The bulk of the bank's revenues comes from standard lending products. The bank's nonperforming loans increased to 1.7% of gross loans as of June 30, 2012, from 1.6% as of Dec. 31, 2011. We expect Eximbank's nonperforming assets to increase due to the bank's history of above-industry-average growth in loan disbursals and its still unseasoned portfolio. We note that Eximbank has taken steps to improve its risk management systems and reporting standards. However, full implementation will take some time. We consider loan quality in Vietnam to be generally weak after taking into account the operating conditions, a substantial lack of information on borrowers, the evolving risk management practices of banks, and the country's rapid loan growth in recent years. Accordingly, we expect Eximbank's asset quality to remain weak by international standards.

Eximbank's ratio of loans to customer deposits of over 100% is higher than that of peers. We expect the bank's deposit base to grow on the back of its branch expansion plans and existing branch franchise. The bank's holdings of cash and other liquid assets support its "adequate" liquidity profile.

Outlook

The stable outlook reflects our expectation that Eximbank will maintain its financial profile and temper growth amid difficult operating conditions in Vietnam.

We could upgrade the bank if it sustainably improves its business position while managing risks.

Conversely, we could lower the ratings if the bank expands aggressively or mismanages risks, such that its: (1) weak assets increase above 10%; (2) liquidity and funding profile deteriorate, such that the ratio of customer loans to deposits remains above 115%; (3)capitalization weakens substantially, such that the bank's risk-adjusted capital ratio before diversification falls below 3%.

Standard & Poor's