Fertiliser sector envisions sunny prospects

Fertiliser sector envisions sunny prospects

Businesses in the fertiliser sector expect rosier horizons ahead amid a number of favourable factors globally and domestically.

From early this month, the hint that several major urea fertiliser makers in China have ceased the signing of new export contracts under request from Chinese government has cast a remarkable impact on the global fertiliser market.

As China is a leading urea fertiliser producer and consumer, its restriction on urea fertiliser exports might tighten supply of the product and significantly push up fertiliser price.

Nguyen The Minh, director of Retail Research at Yuanta Vietnam Securities JSC, noted that China has mandated several fertiliser firms to temporarily halt urea fertilser exports following a spike in fertiliser price in this market, which could extend upward price momentum in the global market, with Vietnam no exception.

Morocco is another country among the top performers in fertiliser exports, but was hit by the most tragic earthquake in the century on September 8, which has cast a big influence on the global supply in the short term.

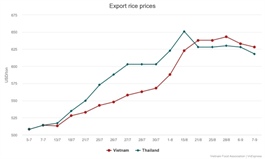

Such events have aided upward price momentum of urea fertiliser in the global market, buoyed by diverse factors such as escalating tension in the Black Sea, a sharp jump in the demand from India due to a shortfall in their domestic production and rising rice growing area, as well as a 30 per cent gas supply cut feeding fertiliser production from Egypt.

Last year, Egypt accounted for 4 per cent of urea fertiliser production volume and 8 per cent of exports globally.

On trading on September 8 alone, urea fertiliser prices fetched $452 per tonne, up by half compared to late June.

In the domestic market, urea fertiliser price is forecast to spike in the fourth quarter of this year.

In the stock market on September 8 the tickers of fertiliser firms responded positively when a raft of tickers ended violet, reaching their peak price in the section.

BIDV Securities JSC predicts that the fertiliser sector would acquire positive prospects in the rest of 2023. The fertiliser price in the domestic market will likely extend growth momentum to keep abreast with that in the global market.

The urea fertiliser price can touch $0.48-0.49 per kg, equal to a 25-30 per cent jump compared to the bottom level in early June.

Amid the resumed urea fertiliser price, PetroVietam Ca Mau Fertilizer JSC (DCM) has eminent prospects for improved revenue and profit due to augmented demands for the summer-autumn price season in the central region, as well as the winter-spring rice season in the northern region.

In addition, DCM’s export prospect is forecast to resume strongly in the second half compared to low base in H1, leveraging the many positive factors.

PetroVietnam Fertiliser and Chemicals JSC (DPM), the producer and trader of Phu My brand fertiliser, they have pushed their output to a maximum to serve soaring demand from farmers.

In the year to date, DPM launched 640,000 tons of Phu My nitrogenous fertiliser into the market and 90,000 tons of Phu My NPK fertiliser.

For the rest of 2023, the company aims to provide the market with additional 500,000 tons of Phu My fertilisers of diverse kinds, holding expectations of apparent improvement in their business results in this H2.

In the case of Binh Dien Fertiliser JSC (BFC), in Q3 of 2023 the company counted $78.8 million in revenue and $2.78 million in pre-tax profit, 10 times more than a year ago.

BFC secures the largest market share in NPK fertiliser production in Vietnam, particularly in the southern region, Vietnam’s major rice growing area.