HSBC: Emerging market output falls in July

HSBC: Emerging market output falls in July

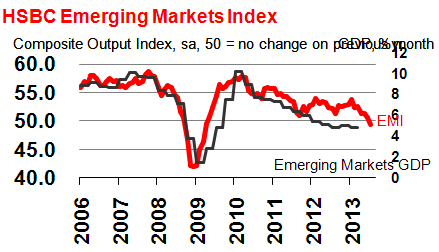

- HSBC Emerging Markets Index: 49.4 (prior 50.6)

- Manufacturing outputdeclines, while services activity stagnates

- Asian manufacturing remains weak, while goods production also falls in Russia, Brazil and Mexico

The HSBC Emerging Markets Index (EMI), a monthly indicator derived from the PMI™ surveys, fell to a new post-crisis low of 49.4 in July, down from 50.6 in June. The latest figure was the first sub-50.0 reading since April 2009, and indicated an overall contraction of output in global emerging economies.

Output fell across the four largest emerging economies, the first broad-based contraction since March 2009. Chinese output fell for the second month running, mainly reflecting a contraction in goods production.

July data signalled the first decline in new business in global emerging markets in over four years. China, India, and Brazil all posted lower receipts of new work during the month, while growth in Russia was the slowest in nearly three years.

Employment in global emerging markets was broadly unchanged in July compared with one month previously. Job shedding at manufacturers offset marginal growth in service sector staffing.

Inflationary pressures remained weak in July. Input prices rose at the fastest rate in four months, but one that remained modest, while prices charged for final goods and services were broadly flat.

Business expectations

The HSBCEmerging Markets Future Output Indexisa new series tracking firms’ expectations for activity in 12 months’ time. The indexrose slightly from June’s low, but was still the second-lowest figure in 16 months of data collection to date. Manufacturing sentiment weakened for the fifth consecutive month, while business expectations in services picked up slightly since June. Among the four largest emerging economies, sentiment was weakest in China.

Frederic Neumann, Co-Head of Asian Economic Research

“Emerging markets are not yet feeling a lift from stabilizing demand in the United States, Europe, and Japan. For example, manufacturers have seen new export orders contract for a fourth consecutive month in July. There are signs that domestic headwinds for growth are stiffening as well. Total new manufacturing orders fell sharply last month, while new orders for services continue to expand at a disappointing pace.

“The main risk for emerging markets at the moment is that the cyclical downturn in manufacturing and softer service sector activity will ultimately lead to a weaker job market. Manufacturing employment in China, Brazil, Russia, Poland, and Korea, for instance, has already started to decline, with service jobs in most cases still growing, albeit at a softening pace. Deteriorating job prospects could weigh on household spending, thus undoing the lift expected from easing consumer inflation in most emerging markets.

“Some comfort, however, can be taken from the relative stability of the future output index. While it eased back marginally for manufacturers it rose for service providers. This suggests that relative optimism remains among businesses regarding the EM growth trajectory over the coming twelve months. Possibly, this may reflect the view, such as in China, that some policy accommodation could be forthcoming to help arrest the broader deceleration in activity.”

HSBC